Australia’s Big Four banks have forecast significant interest rate cuts over the next 6 to 12 months, which could spark a nationwide property boom. In this analysis, we explore how these cuts, alongside global economic shifts, may affect the housing market.

It's official—the banks are coming out here in Australia and suggesting that we're not just going to have one interest rate cut; we're going to have numerous cuts over the next 6 to 12 months.

Now, when those interest rates cut, there are expectations that the housing market will absolutely take off.

If you're interested in my deep dive analysis of what I think is actually about to happen, then definitely keep reading…

Banks Predict Rate Cuts!

The Big Four banks in Australia are coming out and saying home loans are going to start cutting, and they're going to start cutting a lot sooner and a lot deeper than most people think.

We still have so many people out there thinking that inflation is still really high, and for that reason, we can't have interest rate cuts.

However, inflation is only one part of the puzzle, and we also need to know it's not a number we just see today—it's the number that we see trending from the last 6 months. It's the same mistake that the central banks made when it came to inflation going lower when they were forced to keep rates where they were, instead of cutting them.

Now, we've made the opposite mistake, which is keeping interest rates elevated while inflation has been dropping a lot faster than expected.

In saying that, nobody likes inflation, so I'm glad that they did take an approach where they kept interest rates higher. But unfortunately, the cost of that is a per capita recession here in Australia, and a lot of people are really struggling with their home loans.

Now, what the banks are saying is maybe we aren't going to have to suffer for too long.

An expected barrage of interest rate cuts next year could reignite another nationwide property boom, experts claim.

The cuts have reportedly been predicted on forecast drops in the United States’ interest rates, increasing the value of the Australian dollar relative to the Greenback and putting the Reserve Bank of Australia (RBA) in a better position to drop the cash rate.

This is something that you need to consider: it's not just what the RBA here in Australia is going to be doing. While they want to focus on inflation here, they also need to understand what's happening overseas.

How Big Banks’ Rate Cuts Could Trigger the Next Property Boom

If you think about it:

If we suddenly see interest rates drop around the world relative to our Australian dollar, our Australian dollar goes up in value because now it becomes more attractive for people to bring that money into Australia.

What that does is it means, yes, we've got all this money coming in, but our dollar is more powerful. Although people that want to travel would love that news, it is actually quite bad news when we are trying to export things out because it's now more expensive for people in the U.S. and other parts of the world to consume our goods. So, while we sit here and think about our home loan rates, there are so many other things that play a part in the decision-making process.

Now, I'm not sure when you're reading this, but you're probably going to have found that the Federal Reserve Board (Fed) has now cut rates, and it's the first cut they've made in over 4 years. So, that is then putting further pressure on the RBA to start making moves as well.

When it comes to interest rate cuts, it's not just the U.S. that is cutting rates—other developed countries are also doing it.

We're starting to see multiple central banks start cutting rates.

Some people go out there and say it's a massive conspiracy theory—all these people sit in a room, and they say: Now we're going to hike, and everyone hikes. Now we're going to cut, and everyone's going to cut."

What we learned back in school was globalisation and how every economy is now, unfortunately or fortunately, connected. That's why when we find that there's going to be pressure overseas when it comes to a market crash, everyone else will start to feel some of that.

Now, here in Australia, we are somewhat insulated, but we are definitely not going to stand by ourselves when it comes to the market crashing if it happens around the world. We may be insulated and not have as much of a deep correction, but we still will have that correction. The same applies to when interest rates cut around the world. It's evident that they're starting to make their moves, and Australia will soon follow.

The report also added that:

T

his is important to note:

While a lot of us are sitting there saying: "Oh, I'm waiting for interest rates to cut because then if they cut, I can finally get into the property market as a first-home buyer or someone who doesn't own any assets at the moment," you might be able to get in because your servicing allows you to borrow more. But that could also mean that you're having to save a lot more as a deposit to get into that property.

Let's say, for instance, you want to buy a $500,000 property, and you suddenly see a 10% increase in the price of that property. You're now having to save more as a deposit to get in. So, your barrier to entry, although it looks lower because your borrowing capacity goes up due to interest rate cuts, it is actually pushing you even further away from purchasing property.

Going back, according to Louis Christopher: “There is a strong history of rate cuts stimulating housing demand,” noting that the new rate cuts would unleash a lot of pent-up demand from buyers.

Four cash rate cuts next year would mean that the Reserve Bank board is making a decision to cut rates at four out of the eight meetings it's scheduled to have next year.

The report also revealed:

I can tell you now, you're getting prices a lot cheaper than that when it comes to interest rates.

A lot of this, but all it means is that we may have interest rate cuts.

Now, interest rate cuts by themselves may cause some more pressure because there's more demand in the market and supply is not there, but that's only one part of the equation.

Understanding Supply and Demand in the Housing Market

If supply is continuing to go up during that time as well, you won't really see prices go much higher.

However, the latest data that's coming out when it comes to how much supply is in the market and how much is coming in the next 12 months is amazingly low, and that's not just my words—there are experts out there suggesting that it's amazingly low.

We're not going to hit the targets that the government had put in place, and if we do, it's going to be some sort of miracle. It'll be through high-density apartments. They're basically cardboard boxes that they're going to put up in the sky, and that may be your only choice to be able to purchase property and live in one.

Now, I still think in 2024 and 2025, it is still possible to go out there and build to get to the dream home.

A lot of people try to go and get there straight away, or they might buy something that they live in and then say: Well, the next home is our dream home.

This, unfortunately, is a strategy for losers. It doesn’t work. Now, it may work for one in 100 people, but for the majority of you watching right now, it's not the way to do it.

Stop listening to people that suggest, "This is the only way to do it."

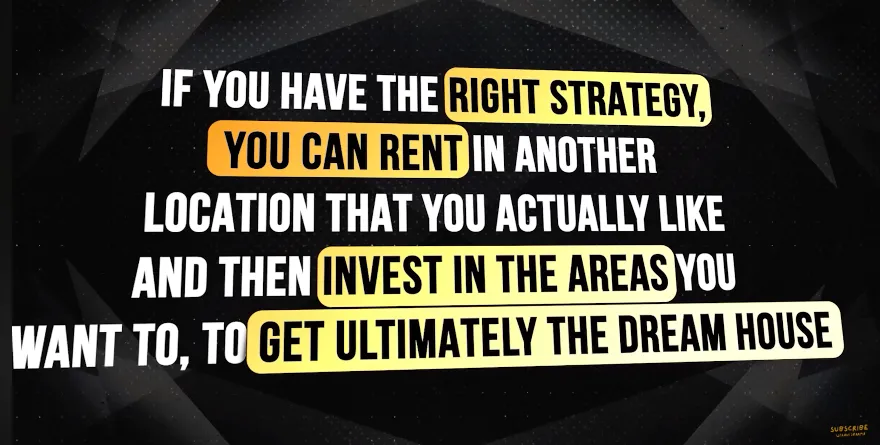

One of the greatest strategies, which takes the least amount of effort, is rentvesting.

I've got a video that you should definitely go check out. It's a strategy broken down, and it's exactly what I'm using to buy my dream home in Sydney, which will cost a couple of million bucks. However, I'm okay with that because it allows me the choice to live where I want, enjoy my life in my 20s, 30s, and 40s, and it'll also mean that I can get the dream house without having to compromise on my lifestyle.

I hope you guys have learned so much from me in this article!

I'll catch you guys in the next one.

Thanks, guys!

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.webp)

.png)

.png)

.png)

.png)

.png)

.png)