Is $1,000,000 Enough To Retire In Australia? | ETFs & Australian Real Estate

With inflation eroding purchasing power, is $1 million still enough for a comfortable retirement planning in Australia? This article explores the limitations of relying on ETFs and index funds alone, breaking down what you need to know about the real value of your retirement savings and why diversifying into real estate can be crucial to staying ahead. Learn why thinking bigger and acting now is essential to securing your financial future.

You've probably already heard about the dollar-cost averaging method into index funds or Exchange-Traded Fund (ETF) to ultimately get you to about a million dollars by the time you retire.

Now, although that sounds amazing, in this article, I want to break down:

What a million dollars actually means at retirement;

Why I think you're going to be quite scared by this strategy and the results; and

Why do you need to start acting now.

If you're interested, keep reading…

A Million Dollars Isn’t What It Used to Be

Now, it's obviously an amazing thing to know that you can become a millionaire by simply doing a few small things. I'm not discounting the fact that this is a real, viable strategy that will get you to a million dollars.

However, is the 4% Rule going to be enough for you to retire?

Now, you might be 50 and looking at this strategy and thinking: By the time I turn 60, which is in 10 years, I'm going to have a million dollars. A million dollars is plenty because I can use the 4% rule, which means you can extract 4% out of your entire holdings, allowing you to live on forty thousand dollars a year.

If you have a house paid off, forty thousand dollars is huge—it's amazing! But, if you're someone that's young, in your 20s, 30s, 40s, or 50s, and your goal is to have a million dollars in the bank account or in ETFs or shares to receive a dividend or some sort of yield, you might be in for a shock.

As you know, inflation is a real thing, and apart from the fact that over the last two years you've suddenly become interested in economics and the property market because everything seems to be exploding at the same time, inflation has always been a concern for a long period of time.

Here in Australia, the inflation target for the Reserve Bank of Australia (RBA) is 2-3%, but how often are we actually hitting those numbers?

Well, the inflation rate in Australia has averaged 4.88% from 1951 until 2022.

Now, we already know that in 2023 it's a lot higher, so that average would be skewed slightly, but it's going to be about 4.88%.

So, why exactly is this important?

What I'm about to show you is an inflation calculator. This got me scared, and I'm actually out there buying assets. I got scared for a lot of people around me who are doing this strategy of: Hey, how do I get to a million dollars, and then I'll be sorted? When in reality, you can actually make the moves now.

Take a look at this inflation calculator. What we're trying to figure out is, what is a million dollars actually going to buy you?

We know what inflation is, so we can reverse engineer and see how much would be enough for us to live a comfortable lifestyle at that point.

What we've got here is: $100 in 2003 would actually be worth $159 in 2023.

This doesn't mean you made $59; in fact, it's the opposite. It's saying that $100 could have bought you $100 worth of goods in 2003, but 20 years later, to buy the same $100 worth of goods, you would need $159.

Mind you, this is just based on 2.69%, which is what this actual inflation calculator has figured out is the average. This, again, is basically for the United States; it's not based here.

Now, we've got to input what we think the inflation rate is going to be. So, if we looked at historical data at 4.88%, what's it going to be worth in 30 years from now?

Most people are going to be working for at least 40 to 50 years, but in this case, we're putting a 30-year window, and we want to figure out what $100 worth today would buy us in 30 years' time.

So, in this case, $100 today would be worth $418 in 2053, meaning the same $100 worth of goods would now cost $418 just to buy the same amount of goods.

Now, this probably isn't going to make a huge amount of sense until we put the million dollars there.

Everyone's trying to achieve a million dollars, so what does that look like?

Therefore, what I'm going to do is change what that figure looks like. A million dollars in 2053 will still buy you a million dollars' worth of goods.

However, if we're starting today, what would it actually be worth in today's value? That would work out to be $239,453. That, to me, doesn't sound like financial freedom. In fact, that would scare the sh*t out of me.

It basically means you've lost about 76% of your purchasing power.

This is why we hear rich people saying: Oh, cash is trash; you should invest in assets, because if you were simply saving your money and had a million dollars in the bank account, you would have effectively lost 76% of your purchasing power.

Now, that is definitely scary.

What's scarier is that you might be in your 20s, 30s, or 40s, where you can actually make a difference. But if you didn't read this article, or you haven't come across these investing terms or didn't even know that inflation was going to eat up so much of your purchasing power, you're basically saying: Well, I think it works because I heard some people doing it, so let me go do the same thing so you go ahead and do what you need to do.

Same thing with your super. You're probably like: Oh, okay, cool, I'm probably going to end up with about a million if I'm lucky, but I'm probably going to end up with about $500,000. That's okay, my partner and I—$500,000 each—is going to be sweet.

However, you're going to get there, and it's only really worth about $240,000 in today's value.

This is scary because you can actually do something about it now. But by the time most people realise this, it's too late. They can't change their habits, they can't suddenly say: Oh, well, I'm going to make an extra two million dollars because that's how much I actually need. No, because at that point, you're not at your peak earning potential.

That's why we have such a big crisis with pensioners not having enough money, especially with inflation being a lot higher than what's actually being accounted for.

Believe it or not, 2 years ago, inflation was a thing, but before that, inflation was always a thing. It just wasn't being documented; it wasn't being promoted in the media. People weren't talking about it because inflation's boring—I don't really care about that.

However, now that it's come to the forefront and we know interest rates are rising, people are questioning, "Why is it rising?" That's because of inflation, and that now is compounding, because once we're aware of these things, we need to start actioning them.

How many people actually take action? Not many.

If you've gone out there with this strategy in mind that you're going to invest or dollar-cost average to get to a million dollars, well, we know it's not going to be enough.

Beat Inflation and Secure Your Financial Future

So, what's the solution here?

Well, I have no idea what your situation looks like, but if you need help around your strategy or actually want to go ahead and purchase property as part of that strategy, you can visit Search Property and book a FREE discovery call with my team, because we'd love to help you get there.

However, one of the things for me, at least, is how do I beat inflation?

How do I build a portfolio?

How do I know that I can end up with more than a million dollars?

If you are having a retirement planning in Australia with a million dollars' worth, I need to end up making probably about four million in today's terms. I need to probably make four million at that point, so I need to do 4x what I originally thought.

Now, I like to invest in real estate. It's a big part of my portfolio, but I also diversify into things like crypto and trading cards and collectibles. So for me, I'm diversified in that way, but a large portion of my wealth is in real estate, and this graph here explains why:

This means: Buying at or below cost preserves the real value of capital, no matter the inflation outcome.

Now again, this doesn't work every single year, but there's a trend. This is years and years of studies to show what this means.

What we can see is that, over time, we see asset prices like property go up because the replacement costs—the materials required to actually build the property—are increasing at a faster pace.

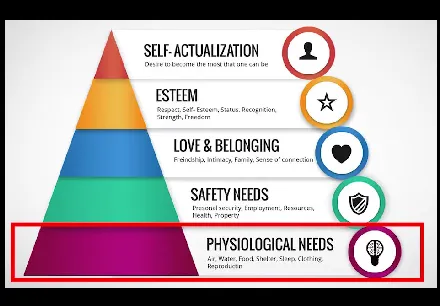

When you've got things like property and it actually sits at the base of Maslow's hierarchy of needs, you've got shelter.

This is why: It is so important that whether people are renting or whether people are going and buying the place, you're getting cash flow and you're getting capital growth.

For me personally, this makes so much sense — to be able to go into something like this, build my wealth over time, and do it with leverage. It's going to get me faster to my goals, which, honestly, have to be so much higher than what anyone else thinks because inflation is a real problem.

Me simply coming out here and saying: Look, you can buy two properties or three properties, you'll end up with a million dollars worth of equity, and yeah, you're sweet, but the reality is that you're probably not sweet.

This is why we need to start thinking outside of the box. The five closest people to you are going to end up in the same position as the majority, and I don't want that for you.

The reason I don't want that for you is because you work hard during your 20s, 30s, 40s, and 50s, only to get sold this dream that saving your money was going to make you rich or let you retire financially free after working for 40 years. I've seen my grandparents go through the same exact thing. They worked really hard, they have their own place, but they live on the pension now. If something volatile happens, like inflation going up, they struggle.

This is why I come from a place of passion and a place to actually help you.

Whether that’s through using my service or not, I just want you to be aware that just because a million dollars sounds great, it’s not what it meant 10 years ago, and it definitely doesn’t mean what it means today versus in 30 years' time.

I hope you guys have learned so much from me in this article.

If you have, share this with someone else who thinks a million dollars is a lot, but in fact, it isn’t — and why you need to start shifting that strategy and thinking bigger because average honestly isn't going to cut it.

I hope you guys have enjoyed it, and I'll catch you in the next one.

Thanks, guys!

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.webp)

.png)

.png)

.png)

.png)

.png)

.png)