My Honest Thoughts On Interest Rates and Property Prices For 2025

Discover my honest take on Australia’s property market for 2025. From navigating rising interest rates to seizing opportunities in an ever-changing landscape, I share insights from my personal journey as an investor and buyers’ agency owner.

Why I would hope for one scenario over the other, especially being in business but also having a large portfolio.

If you guys are interested in what my thoughts are, then definitely keep reading

My Honest Thoughts on the Market

I’m going to talk to you unfiltered. There are no graphs, and there are no stats.

This is completely my own feelings, my opinion of what’s happening in this market, and how I’m personally feeling, being involved in the market, speaking to so many people as well as the staff members that work at Search Property.

I wanted to give you guys an idea of where I think the market’s headed.

Now, I want to provide you as much context around why I think a particular way.

I provide a unique perspective because I not only have a personal portfolio which I’ve been building for almost 12 years in property, but I also run one of the fastest-growing buyers' agencies. So I have to look at the property market with two lenses:

The good news for you is that whether the buyers' agency’s around, whether I’m still buying property or not, I’m still going to be here writing blogs and making videos on YouTube for the next 20 to 30 years unless, of course, YouTube goes, and that’s a whole different conversation.

Now, I started on YouTube almost five years ago, and at that time, I used to have like maybe 10 or 15 views on a video. So the fact that I’m getting now thousands and thousands of views, I also get a lot of questions from you guys, and one of the biggest questions is:

We have these conversations in the office as well because there are people wanting to buy property within the team. They’re trying to buy property. They’re also speaking to people who are asking these questions.

They’re like: What does Ravi think? Because they obviously can’t talk to me directly. So I thought the next best thing would be to come out to you guys and talk to you like we’re sitting at a dinner table and having this discussion.

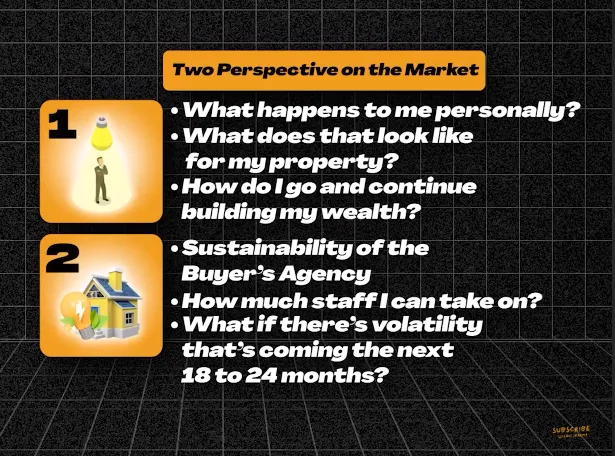

The Two Perspectives on the Market

Now, let’s cover off the two perspectives:

My personal perspective,

The buyers' agency perspective.

Personal Perspective

Personally, I hold quite a bit of debt, but I’m comfortable with it due to my current income level and the gradual, strategic approach I’ve taken to build it over time.

Now, you’ve got to think, the properties that I was purchasing, say 11 or 12 years ago, were about $200,000 to $250,000.

Now, those same properties are worth sort of $500,000 to $550,000.

What’s funny is that back then, I used to have interest rates of about 7%.

Now, we're back to square one where interest rates are anywhere between 6.5% and 7.5%.

For me, I’ve gone through the cycle. I’ve seen where interest rates were really low, and that had its own pros and cons. Now, interest rates are pretty much normalised in terms of the long-term average.

Do I think interest rates will come down? Well, I’ll get back to that. But I’ll give you some more context:

To further explain, I’ve been investing in property for the last 11 years. I will continue investing in real estate, being the largest portion of my portfolio. But the portfolio and the direction for which I take has definitely changed. It’s adapted over time. The reason for that is because I’ve gone from working at a job to then working for myself, having different businesses in different industries.

Now, for the better part of almost 5 years running something I’m the most passionate about I’ve ever been in my life, and also more recently with Search Property, we’ve gone from a team of like four or five people 12 months later to have over 4 full-time staff. So that, in itself, has pros and cons as well.

I’m one of the unique few that have a buyers agency, have a real estate company where I’ve actually built my portfolio before I even got into this industry.

The reason I did that was because I felt like I didn’t have enough credibility. I felt like I wanted to go out there, go through the challenges such as:

What are the pros and cons are;

What are the mistakes I could make—and then, eventually, when I did start up my buyers agency, I could go out there and help everyday people like yourself.

That’s exactly what’s happened.

Whereas I think everyone wants to be a buyers’ agent now, and a lot of them have built property in the last 1 or 2 years.

In addition to that, a lot of them are buying property because they’re making a shitload of money through their BA. In that case, it’s not as relatable to you guys because if they’re making $500,000 to $600,000 from their business, and that’s the only way they could go and actually build a portfolio, it’s not as relatable as to when they were working for $80,000 or $100,000 and building a portfolio that way. That, in itself, has its own challenges.

Now, of course, if you’re self-employed, that also has its own pros and cons, but I think it’s just different.

For me personally, after accumulating significant debt and re-entering the market, finally purchasing property feels like a huge milestone. This accomplishment is the result of investing heavily in our business to better assist clients like yourself and create job opportunities.

Now, with the potential for interest rates to decrease, I’m particularly optimistic.

For every 1% drop in interest rates on a $1 million loan, it could generate an additional $10,000 in positive cash flow.

What I mean by that is if you’ve got a million dollars' worth of debt and it’s at a 6% interest rate, that means you’re paying $60,000 a year in interest repayments.

However, if that went from 6% down to 5%, that’s a $10,000 difference or $10,000 savings in this case.

Therefore, if you’re in a property that’s negatively geared by, say, $5,000, if there’s a 1% decrease in your interest rate, you go from a $5,000 deficit to a $5,000 positive cash flow situation.

Therefore, imagine for myself, where I’m holding millions and millions worth of debt, I’d be very incentivised to have the interest rates come down, and I really, really hope they do.

Now, at this point, you’re probably like: Well, that’s sort of expected. Like, I knew you were going to say that—you hold debt, you want interest rates to go down, so that makes sense.

In most cases, with the interest rates coming down, we’ll probably see prices go much higher as well, which again puts me in a stronger position. But this is why I have a unique perspective, because I also run a company within the same industry that I’m largely exposed to as an individual investing in there.

When I flip over to the buyers agency side, I have a view that almost, almost contradicts what I want on my personal front. To a certain extent, even on my personal front, the longer interest rates stay higher, the more time I have to be able to accumulate undervalued assets.

Why? Well, I honestly believe land in Australia is undervalued.

Despite prices having gone up by so much, I still think it’s undervalued mainly because if you’ve gone out there and traveled—I don’t know if I’m biased or not—but Australia is the best place to live in this entire world.

I would go on to say Sydney is freaking amazing, but again, I was born here, and I’ve only ever lived in Sydney. But I have traveled a lot and more recently, I traveled to the US.

I can tell you now that my perspective on traveling to 35 countries over the last 10 to 15 years has told me one thing: home is home. Sydney is by far the best.

However, it comes at a cost, and the cost is that our land and our houses are so ridiculously expensive that it’s so hard to live here. The cost of living has definitely not helped.

When I put that into context, I’m like, well, if things are still undervalued, I would want to go out and get as much as I can so that I can not only feed my family but everyone else in my extended family to give them the life that they couldn’t actually achieve themselves.

I also don't want to put my kids in a situation where they're not going to live close to me, and that would only happen because they can't secure land here in Sydney.

Trust me, I've definitely thought about just moving overseas. I'd be able to save so much in terms of costs, especially from a housing perspective. But to me, I love my family, and I want to be close to them.

The Buyers’ Agency’s Perspective

Now, flipping over to the buyers’ agency side: if interest rates do come down, it will mean that so many people sitting on the sidelines will finally be able to enter.

There are a couple of groups of people who could enter.

Number 1: People who are scared and can’t borrow.

They think interest rates will continue higher, or because they're so high at the moment, it just makes no sense to get in. In case there's another interest rate hike, they’re thinking: I'm screwed. These are the people who can borrow but just don't want to enter.

Number 2: People who can’t borrow but really want to invest.

This might be you. The majority of people are waiting on the sidelines, having seen prices go up. They want to get land, they want to get houses, but they're like: I can't because interest rates are so high. I can't get a loan from the bank. Because of this reason, there is so much demand sitting on the sidelines that is going to enter when interest rates cut.

From a buyers agency perspective, this could be the best thing ever because it would mean the floodgates open when it comes to clients wanting help. That would mean huge amounts of demand.

However, is there going to be enough supply?

A lot of people might just go: Well, I don't want to sell my house anymore. Interest rates have started cutting. I might find myself being able to hold this for much longer. I might also feel like, hey, prices probably go up because interest rates are lower, so I'm just going to continue holding.

What that means is it dries up any available supply. So, we can't go out there and actively source property. If we do, we're probably having to pay way above market value just to secure something.

A lot of other buyers agencies are already in this situation. They're struggling to source property. I've seen some of the deals we're going up against with these other guys, and they're paying way above market value just to secure something.

If you think about it, for us, on average, we would get a client in and out within the system of purchasing a property from the time they sign up within 3 to 5 weeks. That is extremely fast. That's because our relationships are deeper, we have such a good brand, and we have such a good process when it comes to securing a property, getting details across, and having the conveyancer work with us.

There are other buyers agencies—whether they're small one-man shows or other companies that are quite big—that are, on average, finding property between 8 and 14 weeks, which is almost double the time it takes us to find something.

The main reason for this is because supply is a real concern.

If we see interest rates go down, on a personal front, I would absolutely love it because my cash flow goes into a really good situation. Any of the other debts that I've taken out will then reduce in terms of how much I have to pay, and that would put me in a better position.

It probably means that the market’s absolutely ripe. We have the share market, crypto, all going up at the moment, and also house prices moving higher.

From a Buyers’ Agency’s perspective, it will open the floodgates, and we’ll have all these clients wanting to buy. But from a supply side, we may not be able to find what we need to find. When I say "we," I mean the industry as a whole.

One thing that could counteract this is that when interest rates do fall, we usually see transaction volumes increase.

People want to sell their homes, downsize, or upsize. They do that when interest rates go down. They also do that when there’s certainty in the market.

When we find ourselves in a position where inflation’s been tamed, and we get to normal times—even if interest rates drop by 100 basis points and we sit at an average of 3.5% or 3% in terms of a cash rate, meaning interest rates are probably closer to about 4.5% or 5.5%—I think people will be okay with that.

I don’t think anyone right now is sitting there expecting interest rates to drop back down to 1% or 2%.

As soon as we have a lack of volatility in the market, I think that’s when we see the next leg up because people will transact a lot more.

One of the biggest things that, although on a personal front, absolutely killed me is that I couldn’t get a loan at certain times. I also know others couldn’t get a loan, with the Australian Prudential Regulation Authority (APRA) coming in with stricter banking conditions and lending restrictions.

What it’s done is it’s made our foundation here in Australia a lot stronger when it comes to houses, home loans, and how they’re allowing people to purchase property.

Having the buffers in place—not just from APRA but also from banks themselves when it comes to their calculators—I think is actually a really good thing because it means the foundation we can build off for the next leg in terms of prices going higher is more sustainable.

I’m also in a unique position because I own real estate as an investor, but I also rent.

On the flip side, I’ve seen my rent increase by a lot. I just got an email yesterday saying they’re going to increase my rent by more than 20% on the next hike.

From the time I moved into this apartment to now, where I’ll probably end up, is going to be an additional 40% increase in just three years. So, I definitely feel the pain when it comes to high interest rates, not enough supply, and being a renter. I can see it from that perspective too.

I hope you have learned something in this article.

Thanks, guys!

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.png)

.png)

.png)

.png)

.png)

.png)