In this article, I share essential lessons on common financial mistakes that people make, which can keep you poor forever. Whether you're in your 20s or just getting started on your financial journey, understanding these traps is crucial. From career choices to the influence of your social circle, I'll guide you through avoiding these pitfalls and setting yourself on the path to financial success.

I would definitely not be as wealthy as I am today if I hadn't learned from other people's mistakes.

In this article, I'm going to share some insights on the common mistakes people make and the traps you should avoid if you're aiming to be financially free.

If you're interested, keep reading…

Harsh Life Lessons

I came across an article with the headline:

Upon reading it, I thought, Hey, that seems pretty interesting. Let me see what this article is about.

They shared a few key lessons that most people should know about.

I appropriated them—I took the article and thought, Instead of you having to read through some boring content, why not make it more interesting? So, I’ll not only share what the life lessons are but also how we can apply them in Australia to benefit you.

Although this article targets people in their 20s, I think it’s relevant to anyone who is young. So, anyone under 40, in my opinion, is young when it comes to building wealth.

Now, if you're over 40, and we have some clients who are over 40 that we help out, it doesn’t mean you’re old. It just means you’re at a different phase of life, and many of these strategies or concepts we discuss may not apply to you in the same way. We just need to adjust them, which is easy to do.

This article is aimed at everyone under 40, but if you’re over that age and have kids, this is definitely one you’ll want to read.

First Lesson: Super Linear Jobs are Often Competitive and Crowded on the Way Up

The first thing you need to learn about is:

In addition:

What does that even mean?

Well, it essentially means that if you’re picking up skills for a job that’s pretty broad-based, like an admin job or something entry-level, it’s extremely competitive to find and keep that job.

Additionally, it’s a field that could easily be replaced by someone else or Artificial Intelligence (AI). This is a topic that’s being discussed every day when it comes to AI and its impact on many industries. This category is probably where it will have the most significant effect.

Therefore, if you’re going into a cushy job or something that just pays the bills, that could be great to get into. But once you’re there, you know it’s very competitive. Increasing your income will be much more difficult because your employer knows that if you don’t want the job, someone else does.

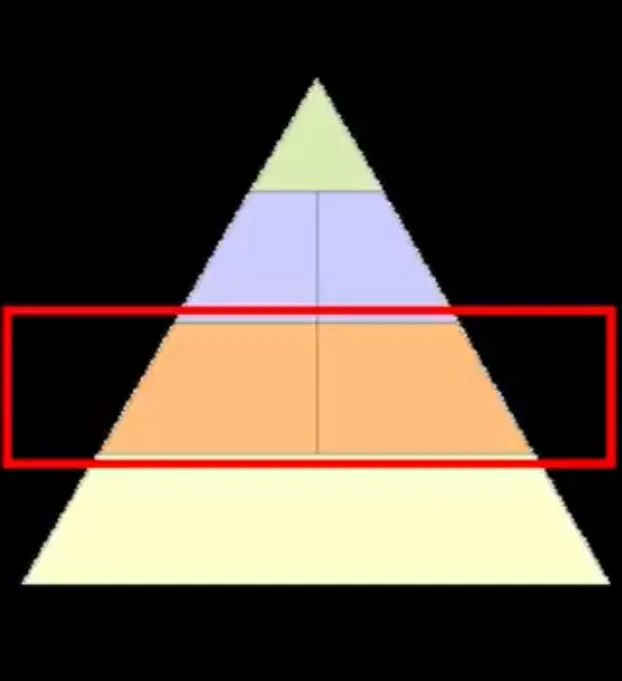

Think of it like a pyramid.

At the bottom, you have the most candidates who can do that job because it requires basic skills.

As you move higher up, you have the more desirable roles that require talent or a strong work ethic. Getting to that point is much harder.

However, when you get there, it’s harder to find a replacement, so employers will pay you more, especially if you’re considering moving from one company to a competitor. They’ll pay you what you want.

When it comes to increasing your wealth over the long term, you ideally want to upskill from the bottom of the pyramid to the top, because that’s where you’ll make the most money.

However, it doesn’t necessarily mean the highest level of happiness, so always take this with a grain of salt.

Second Lesson: Be Willing to Fight Tooth and Nail for it Before the Age 30!

The second lesson to learn about is:

Now, given that I’m currently 30, I can definitely attest to this. I know that for myself and my partner, we could spend hours and hours at work all day, every day if we really wanted to, because our level of commitment to kids is zero—it’s not active because we don’t have kids.

In addition to that, if you’re out there with:

Kids, and

Multiple jobs,

You need to factor in all these things before making a financial decision. It really does hold you back.

When you’re working at your job, you also need balance in life. You might think: Well, I need to consider the needs of four or five other people I live with before making a decision.

Versus…

If you’re single and in your 30s, you’re probably willing to go above and beyond—eating two-minute noodles every day, going out there, and actually building your business or working on that side hustle.

I’m sure a lot of people in your life have told you, “Start when you’re young.”

Why? Because as you get older, your level of commitment also increases. If you have big aspirations, you need to move fast. The same goes for building a property portfolio—the earlier you start, the bigger the benefit.

Third Lesson: Your Friends and Family Do Not Always Know What is Best for You

The next lesson to keep in mind is:

I agree with this so much because I've seen it in my own life personally. Not only have I experienced it, but the people closest to me also experience this regularly.

If you take a step back from just the finances, you’ll realise that your friends and family love you (hopefully they care for you), and that’s why they’re your friends and family, and why you stay connected to them.

However, their main intention is to keep you safe because they care about you. But what often happens is that people get held back because of their own experiences.

For example, I’ve dealt with many people who are very fearful of making a move in property. They’ll never go and buy a property because their parents may have lost money on a bad investment—or even worse, you might have friends who say, “Well, I don’t really agree with that. I’ve got a different mindset. I want to do X, Y, and Z.”

This is why you often hear that you're the average of the five people you spend the most time with. If you hang out with people who are content making sixty thousand dollars, renting for their entire lives, and don’t really care if they have to move at some point because they can’t afford to live in that city, well, that’s great (if that’s what you want too).

However, if you actually want to live in Sydney, near the beach, and own a five or six million-dollar house, those friends aren’t going to really push you toward that goal.

This is why you need to align yourself with the right people in your circle.

Another part of this lesson is that you’ll get advice from people who don’t really know what they’re talking about.

For instance, a couple of years ago before I started the YouTube channel, I used to get a lot of advice from this uncle.

Everyone has one of these uncles (or it might be an auntie) who thinks they’re very successful, even though they’re not that successful.

Anyway, he came to me and said, “Oh hey, you should do this when it comes to property investing.”

At that point, I had bought a few properties. I was constantly learning, but I was open to listening. So I asked, “What exactly do you suggest?”

Then he told me he only had a one-bedroom apartment, and I was like, “Okay, and what else?”

I also thought, “Am I better off listening to you, or am I better off reading three or four books from people who have successfully done this and learning from people who are actually living the life I want to live? Wouldn’t I get better results that way?”

Therefore, you’ve got to put emotions aside.

You’ve got to focus on logic because, at the end of the day, yes, friends and family do care for you, but they’re not always the best source of advice when it comes to things like property investing or life in general, especially if they have no experience in that field.

4th Lesson: Money is Important

The next lesson is simple:

Let’s not beat around the bush.

Everyone talks about how money doesn’t buy happiness.

People might say, “Ravi, all you think about is money.”

But on the contrary, I think about a lot of other things because I don’t have to worry about money—I made it a priority. I still make money a priority, but it takes up a lot less room in my head because I’ve set up systems, and the machine I’ve built allows me to make better decisions overall.

So when people say money isn’t important—it is very important.

It’s important that you get it right and prioritise it. If you can prioritise this for yourself when it comes to working or learning a new skill, it definitely needs to be a priority because you don’t want to end up studying for 10 to 15 years, racking up student loans, only to get into an industry that pays you minimum wage. That will set you back significantly.

Financial stress is one of the worst kinds of stress you can experience, and I’m sure it causes a lot of marriages to break down. So, it’s one thing you definitely need to prioritise.

Once you get that part right, you just need to tweak it every year as you enter new phases of your life, and you’ll be set for the rest of your life.

Last Lesson: Life Changes Slowly, Unnoticed Until a Setback Occurs

The last lesson is:

We often overestimate what we can achieve in a year but underestimate what is possible in two to three years.

I really love this lesson because when you’re building toward something, whether it’s a machine or personal development, it takes time. But we tend to think, “Oh, I’ll build all this stuff in two weeks or six months, and then I’ll do X, Y, and Z after three or four years.” We overestimate what we can do in the short term but underestimate what we can achieve over a longer period.

For example, if I wanted to save $100,000, I might think I could get to maybe $75,000 in a year. In reality, I might only get to $40,000, but my longer-term goal is to have $200,000 after five years.

I would likely have a lot more than $200,000 in that longer period because I would have invested that money, and the compounding effects would have worked in my favor.

However, our minds work in a very strange way. The main takeaway is that if you’re creating goals for yourself, don’t be so hard on yourself in the short term, but be extremely ambitious in the long term. Chances are, you’ll absolutely blitz your long-term goal, even if your short-term results disappoint you and throw you off track.

I know this lesson holds a special place in my heart because it’s always happened to me. When I started buying property, I thought, “Oh, I could probably buy X amount in two years, and in 10 years, I might be at Y amount.”

However, in the short term, I didn’t quite hit those targets, but in the long term, I exceeded them by two or three times. So, keep this in mind as you set goals for yourself.

I hope you guys enjoyed this article. I know it's a bit off-topic from the usual Australian real estate content because, hey, we’re talking about personal finance and mindset. If you're interested in more content like this, definitely subscribe to my YouTube channel or continue reading my other blogs.

I'll catch you guys in the next one.

Thanks, guys!

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.webp)

.png)

.png)

.png)

.png)

.png)

.png)