What Will Happen If Negative Gearing Is Removed? | Property Prices

The debate over negative gearing in Australia is heating up. What happens if it's abolished? In this article, we break down the possible effects on property prices, rental markets, and investment strategies. While some may fear the loss of tax benefits, savvy investors could seize new opportunities. Stay informed and understand the real risks and rewards of this significant potential change.

The politicians have said they're not going to touch it, but now they're touching it, and everyone's getting a little suspicious.

Now, if you're here for the short answer, what does this mean?

It means:

What’s the effect then?

Well, if rents skyrocket, that plays into the whole inflation narrative, which means inflation goes up again.

How can you cut rates during that time? Well, that's why we're going to break it down, and I urge you to stay all the way through this article because there are things here that will affect you not just in purchasing property today, but also, if you're someone renting property in one of these markets.

You need to pay attention because it could mean big changes for you.

I will preface this conversation by saying: I personally don't think it's going to happen.

The reason I say this is because there have been countless times where the topic of negative gearing has come up, and changes or at least the abolishment of negative gearing in Australia have been discussed over the last 10 to 15 years.

A lot of you may not have even wanted to know about property 10 years ago, but I've been investing in real estate for about 11 years, and even before I started, there were already conversations about negative gearing and how it was going to change.

The reality is, it hasn’t changed, and there's a reason for that.

If you think about it:

If I have negative cash flow, which essentially means the income I generate from my rent is lower than my expenses for holding that property, it could mean I’ve got insurance, council rates, water rates, and the biggest expense, my interest repayments on the mortgage. If that number is higher than the income I generate, it means it's negatively geared—negative cash flow.

Here in Australia, the government has incentivised people to buy property by saying, "Look, we’ll help you out. You're buying property, which is great for the economy, so we’re going to reward you by allowing you to claim that as a deduction on your tax."

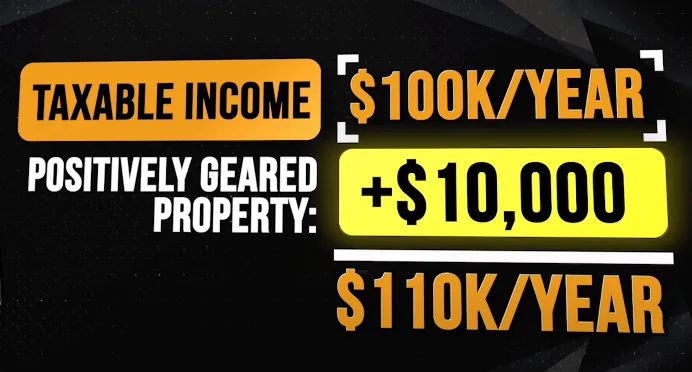

Now, how this works is, if I make $100,000 a year as my taxable income, and I have a property that is negatively geared by $10,000, the government allows me to say: You don’t actually make $100,000; you make $100,000 minus $10,000.

This means they tax me at $90,000 instead. That's a simplified version of how it works.

Positive gearing or positive cash flow is the exact opposite. If you make $100,000, they tax you at $100,000.

However, if you have a property portfolio making you $10,000 a year, you’re really making $110,000, and they’ll tax you on that.

Straight away, negative cash flow sounds good because I can reduce my taxes. This goes back to the age-old argument:

Once you understand that, you’ll eliminate 90% of the poor choices, such as house and land packages, new builds, and off-plan properties, because they're all bullsh*t.

What you want to focus on is, "How do I build wealth?"

The tax benefits and everything that comes with that are all positive—that's all a bonus.

Right now, I want to focus on the best properties and the best locations to build wealth. That’s what I’m doing.

If we did remove negative gearing, the benefit I’ve just explained goes away. It means that people can no longer claim against their taxes, and the real fear here is that people think if we remove this, investors will have no incentive to hold the property.

To a certain extent, that’s correct. Because if you simply bought the property to reduce your taxes, guess what? You’re screwed.

You might say, "Even if the property doesn’t grow, I can save on my taxes because that’s what I bought it for."

This would eliminate so many bad operators in the space because they’re basically selling you something they know isn’t going to grow. They’re just selling it to you because: Hey, you can reduce your taxes, and you love that, because who loves paying taxes?

So, you think: If I can reduce them, I’ll buy the property.

Most accountants go out there and tell clients the exact same thing: buy a property because your taxes are too high. So, you end up buying something new to get the tax depreciation, it’s negatively geared because the rental yield is low, and then you think: Well, it’s okay, you’re holding the property, it’s going to grow in capital, but from a cash flow perspective, you’re saving on taxes.

That is the wrong way to approach this.

What Happens If Negative Gearing is Abolished?

If this change actually comes into effect, a lot of people are going to lose a lot of money.

If you’ve gone down that strategy and bought the wrong property for the purpose of reducing your taxes, guess what?

You now don’t have the benefit of negative gearing, and that means you’re now holding a property for the sake of holding it.

If it doesn’t grow—because you didn’t buy it for growth, you just thought that was going to be a bonus—you’re now holding a dud property that doesn’t give you any benefits, and most likely, you’ll be forced to sell.

If you’re not getting the benefits from the tax break and the property isn’t growing, why would you hold onto it?

That’s why, if this actually plays out, there are so many consequences and one of them is:

I think that the market will see a lot of people lose money because they’ll rush for the doors, trying to sell at whatever cost.

On the flip side, if you’ve bought property for the purpose of building wealth, chances are that within the first two to three years, it’s positively geared anyway.

The takeaway here is that it really won’t affect you.

Negative gearing wasn’t part of your strategy anyway—you’ve bought the property, it’s positively geared, and you’re making money.

This is exactly my strategy: buy for capital growth and buy for cash flow.

Why would you want to lose money just so you can earn some of your tax back?

Even with that concept, you’re saying: I don’t want to make an extra dollar, which would mean more growth and more rent, because I don’t want to pay 30 cents, or I don’t want to pay 45 cents.

But in that example, you still keep 55 cents, right? Most people are approaching this the wrong way.

This is why if negative gearing is abolished, you’re going to see more demand for properties that make sense, driving prices up in areas with an undersupply of properties.

Investors won’t leave their properties; they’ll likely double down, meaning more owner-occupiers can’t buy, and rents will rise in those areas. It will ultimately come down to the whole idea of undersupply and oversupply.

If you have more properties to rent, you're probably going to have lower rent.

However, right now, vacancy rates in Australia are at historic lows, and something like this, which is such a major change, could completely wipe out dynamics in certain markets and really push rental prices in other locations.

Now, some investors are relying on negative gearing to be able to hold that property for longer.

If you realise that you’d get no benefit on the tax front, you're now finding it really difficult to hold a large portfolio.

Therefore, what you could see is people holding multiple properties in their portfolio, who are getting some of the tax back. If they can no longer get that, they will now have to reduce how many properties they can hold.

This is why it's so important to have the right strategy and execution, because what’s worse than buying the property is having to sell it, along with the transaction costs that come with it, especially if you've made no growth.

Now, I do think abolishing negative gearing, although it has its pros with some people saying: Well, now investors will be out, I can buy my own property, it also means:

The reason for that is the incentive for someone to build new and get the tax benefits is really gone now, and they might say: Well, what’s the point of actually buying something new? I might buy something existing, and developers might go: Well, we have no demand, so I'm not going to build more houses.

If you have no houses, which means incoming supply is reduced, you're going to end up seeing prices go higher.

This is the opposite effect of what people think is going to happen.

So, you've really got yourself a situation where rents will probably go higher for quality assets in quality areas, and you’ll probably have prices go higher, which means the barrier to entry is also going to go higher.

What this is, is a capital gains tax that you pay on the capital gain you've made.

How this works:

Let's say you've purchased an investment, and it's gone up by $100,000, you would get 50% of that wiped away, and you don’t have to pay taxes on that, and that's if you hold the property for longer than 12 months, and it's under your own name.

Now, although I look like an accountant, I'm definitely not an accountant, so you'll have to speak to them specifically about your tax situation.

What happens if the 50% CGT Tax is removed?

Well, what it could mean is that people could hold onto their properties for much longer.

A lot more people will also buy their own property because on your own property, you don't have capital gains tax. So, you now have a situation where people will most likely buy their own home, which is against what I advocate for, which is to invest first, invest well, and then make all the gains to be able to buy your own place—you have more choice.

People are now going to become mortgage prisoners, which is maybe what the government wants.

On the flip side is, if people now have to hold on to properties because they don’t want to pay the taxes, that means it’s not a productive economy. You don’t have more transactions going through. Some people want to just downsize, they want to pay off some of their debt—they can’t do that.

If they can’t do that, that means someone else can’t buy their own home. So, you now stop the transactions, and that then has a flow-on effect to the government, who also rely on transactions because they love stamp duty.

All of the taxes involved are something they rely on.

Another thing that could happen if transactions go lower in terms of volumes is that all the people involved in that process also start losing jobs, and that is not what the government wants.

Now, believe it or not, in the 1980s, we actually had negative gearing temporarily removed, and what happened was not the desired effect. That’s why they reintroduced it again.

What happened during that time was that rents actually went up, and it didn’t benefit the people it was supposed to benefit.

So, the theory was that if you remove negative gearing, lower-income earners would be able to get into the property market.

However, the opposite happened, because in order to buy property, you need to have:

What we saw is that in the 1980s, when they did go and remove negative gearing, the rents actually went higher. So, it meant that people couldn’t save enough to be able to purchase the property, and that goes against the entire concept.

Now, one of the things that could happen is a grandfathering rule. So, it might mean that anyone who’s purchased property right now, they might just say: Okay, you’ve got the next 10 years, and we won’t apply these changes to you.

However, after a certain date, if you purchase property, you now have these new rules applied to you.

This has happened before, where they grandfathered certain rules.

This is why, if you are in the best situation to purchase, I don’t know why you wouldn’t purchase. Because if they do change things, they’re most likely going to have to grandfather a lot of these things anyway.

That means you might still have CGT tax exemptions all apply to you as a grandfather rule, you might still have negative gearing benefits for the next 5 years. This is why it’s so important that you get the right strategy and control what you can control.

I know that there were tax laws that were going to be implemented in Australia, and they introduced it in Queensland as a bill that might come through. Because it might come through, people thought it was coming through.

This is similar to how people are approaching negative gearing right now.

You might be convinced that it’s happening, but guess what?

Over the last 10 to 15 years, they’ve tried this multiple times. In the 1980s, they actually did it, and it didn’t work out the way they wanted to.

Final Thoughts

The concluding thoughts I have here are that there is a large percentage of people who might get spooked by this.

The chance of them reading this article is probably next to none, or even if they did read it, they probably won’t do anything about it.

However, if you’re the select few that actually go and read between the lines of what I’m saying here, it means that there is a massive opportunity.

Why? Because I don’t think personally it’s going to happen, and even if it does, it probably affects the markets you’re not investing into anyway, because you’re investing to build wealth, not to reduce taxes.

Now, before you go on to say I’ve got a biased opinion, it’ll actually be more beneficial for me and my clients if negative gearing is abolished. Because if you think about it, we purchase property in the right locations.

Most likely, within 2 years, it’s positive cash flow anyway, so negative gearing doesn’t apply to us anyway. All it will do is further push rent prices in these locations, which means more passive income.

The more demand that comes into this market because people realise they’ve been investing in the wrong way means prices go higher anyway.

So, if I had a personal opinion for the reason of making wealth, it would be that negative gearing should be out, and that would be more beneficial to us. This is where the bias would be. But I don’t think it’s actually going to happen.

If you actually want to buy property for the right reasons, with the right team—we now purchase 80% of our properties off-market.

The industry average of purchasing property through a BA is probably closer to about 8 to 10 weeks, whereas we’re doing it in 2 to 3 weeks because we have the team, we have the relationships, and we have the skills. So, if you’re interested, book a FREE discovery call with my Search Property team, and we’ll make that happen.

Hope you’ve enjoyed this one—catch you in the next one! Thanks, guys.

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.webp)

.png)

.png)

.png)

.png)