Which Is Better? Pay Off Your Mortgage Faster or Invest More? | Australian Real Estate

Should you focus on paying off your mortgage faster or invest to grow your wealth? With rising interest rates impacting cash flow, this comprehensive guide compares both strategies. Learn how to manage debt, build equity, and make informed choices to secure your financial future in the Australian property market.

With the interest rates rising, it can become really difficult to manage cash flow, especially if you have a loan.

In this article, I want to discuss the following options:

Paying down your loan faster; or

Using the extra funds to go and invest further.

If you're interested, keep reading.

Pay Off Mortgage vs. Investing

Now, you might be in the camp of just going: Ravi, I don't care about investing. All I want is my house, and I want to pay it down as quickly as possible.

Why? Because it's probably the largest amount of debt you're going to take on in your entire life. So yes, it does take up real estate in your head when you go to sleep at night.

Peace of mind and having a "sleep at night" factor is very, very important, especially now, with interest rates increasing every month. You're going: Oh no, I've got to pay a little bit extra now. I have to manage the budget. Now, I definitely can't go get Ben & Jerry's ice cream. (Okay, no, that's just me. No worries).

However, either way, everyone is concerned about inflation and interest rates.

There are two things that most people will think about when they're going and purchasing their own place.

"I want a place to stay, and I want to own it, so I don't want to rent."

"I want to create a huge amount of wealth, and I've been told real estate's great."

When you think about these two things, one is emotional, and one is supposed to be rational and logical.

However, unfortunately, the emotions take over.

If you go ahead and buy a place for yourself, your bias will kick in and start saying to you: Yeah, this will grow because I like it, which means everyone else should like it too.

Unfortunately, that's not how investing works.

If you are in the camp of trying to buy your own property to grow your wealth, well, let's discuss what that could actually look like.

Now, we got taught at school: as soon as you take on debt, you should pay it down as quickly as possible. So, if we went ahead and did that, what would that look like for a property in, say, Sydney, Melbourne, or some parts of Brisbane now? Because hey, prices are going up everywhere.

If you do live in Sydney or Melbourne and you've bought a house over the last year or two, you probably paid about a million dollars, right?

Now yes, I'm totally aware that some people can purchase properties for a lot less, but I also know there's people that have purchased for a lot more. So, we're going to use a million dollars as an average.

Let's also assume you haven’t put a deposit down. We're just going to go in and say you've got a million dollars' worth of debt, and that's for the purpose of this exercise.

I'm not a financial advisor. I definitely don't look like one, and therefore, I can't give you every single example. So, use this as a guide to run your own numbers.

Application

If you have a million dollars' worth of debt at today's interest rates of about 5.5%, your interest plus principal repayment will be $5,678 per month, which equates to about $68,136 annually.

Once you include rates, insurance, and any other bits and pieces, you're probably at about $73,000 per year.

Let's take into account what that means.

You've bought a house because everyone told you to buy a house. Now, $73,000 will go into this property just to hold it.

Yes, you're paying some of that debt down as well because you're paying interest plus principal. But for the next 30 years, you will pay $73,000 every single year towards holding this property.

This is why they, you know, sort of say you've got the shackles on, because $73,000 is not a small number.

Now, if you're someone making $98,000 a year, which is basically an average number at the average age of who's watching this—but again, use your own numbers—after tax, you're probably at about $73,000 per year.

Now, you're starting to see why the numbers make sense. That $73,000 from one person is going straight into the mortgage and holding that property.

If you're doing this by yourself, it makes no sense because all of your money is spent on the house, and now you have no money to eat, drink, or watch Netflix.

In that case, it probably doesn't make sense to be spending a million dollars on a property for yourself. But if you're moving in with your partner, then there's two incomes.

Let's assume both people are making the same amount—$98,000 each. That means one person's income is going towards the house, and the other person's income goes towards your expenses and potentially investing.

Once you account for basic household expenditure, assuming $350 a week—again, this depends on where you're living and what your lifestyle looks like—this would be either a ridiculous amount because it’s too high or too low. But let's use $350 a week.

If you've got $73,000 after tax from one person's income, after these payments of $350 a week, you're left with about $55,000 for the year. That's pretty good.

Let's play out the scenario.

If you, as a couple, use $55,000 a year, saying: I’m going to pay down my loan faster. I don't care about savings. I'm going to pay down this loan as fast as possible, what would that look like?

That would be an extra repayment of $4,583 per month, which means your total repayments go up to $10,261 per month. In this case, you would pay off your 30-year loan in just 11 years. Sounds phenomenal—and it actually is—because not many people, if any, will get to this point.

Where it really gets better is if you purchased your property and you're hoping for some growth.

Let’s say you did get lucky and got into the right area, and it grows at an average of 7%.

By the time the property is fully paid off, it’ll be roughly worth about $2.1 million. So, you'll have an asset worth $2.1 million after 11 years, with no debt attached.

It’s actually a really good deal.

Now again, this is based on the fact that you have no savings, you're not spending any money towards holidays, and the only expenses you have are about $350 per week. It also factors in that both people are making $98,000 per year. (Oh, and you have no kids in this example.)

If we assume the same income and expenses, but instead this time, instead of using the $55,000 towards paying down our mortgage, we use that money to go and invest—using it as deposits to buy more property—what would that look like?

After year one of holding that property, your actual property value would have gone up by $70,000 because it's growing at 7%. Your house has gone up by 7%. You'd probably take that out at about 90% LVR (loan-to-value ratio), and you've also saved $55,000. So, you'll be left at the end of the year with about $125,000.

In this case, you decide: I'm going to use the majority of it as a deposit, even though my minimum deposit to get started is probably about $70,000 to $75,000. I'm going to put $110,000 and leave $15,000 as an emergency fund.

So, what would that look like if you went ahead and purchased a $450,000 brick home with the help of Search Property?

We're going to assume about a 7% growth rate.

During 2022, I’m very proud to say that our actual growth rate across the average of all our portfolios for clients was 12.12% in a market where interest rates went up eight or nine times, and the national market dropped by about 7.1%.

When I say it's probably going to grow by 7%, you'll have some years that are higher than that, some that are lower, but I still think we’ll outperform the market if you’ve purchased with the right advice and research.

Personally, I’ve been building my own portfolio for about nine years, and every year, the average growth is at least 11%. So yes, I do have confidence in what I’m doing.

Now, because in this example, we're only buying one property and using the funds from one year.

After year one, we go back to the strategy of using the $55,000 to pay down our loan as fast as possible.

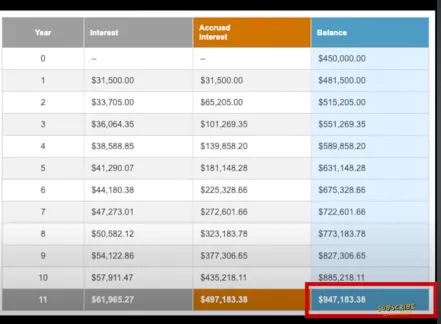

What does that actually look like? Well, the $450,000 property we bought is now worth about $947,000.

Because we didn’t use the extra $55,000 in year one to pay down the debt and took out extra debt (equity of about $70,000), after year 11, you’d have $127,000 of debt left on your house. In the first example, after 11 years, you're debt-free.

Here’s where it gets really interesting: your investment portfolio is now $947,000, having generated $497,000 worth of equity. Plus, it would be positive cash flow. This means, although your debt still exists and is about $120,000, after 11 years, you're probably signing up for that anyway.

If you’ve only got $120,000 of debt but have managed to increase your wealth by about $497,000, net-net, you're still getting further ahead. This is just based on one property.

If you scaled up, what would that look like? If, for four years, you used the equity plus your savings to buy another property four times and then shifted back into the debt reduction strategy to pay off your loan as fast as possible, the numbers become surprising.

The equity in the four investment properties after 11 years would be worth about $3.43 million. Minus $1.8 million in debt, you'd have $1.63 million in equity in the investment portfolio.

Additionally, you’d generate about $30,000 to $50,000 in passive income every year. The debt on your principal place of residence would still be about $600,000.

Essentially, you're saying: I would rather have $600,000 worth of debt plus take on more debt, but that debt takes care of itself with the investment properties. It’s productive, and with positive cash flow, you're not really putting anything from your pocket.

In this case, you would end up net-net a million dollars in net equity, and you would have five investment properties instead of just the one home that you have.

What’s more, you can continue putting down fifty-five thousand towards your actual home loan, or you can use the positive cash flow from the investment portfolio to start paying down your mortgage at a higher pace.

That means after a few years, you’ll have paid off the debt on the principal place of residence, and then you’ll have an investment portfolio yielding passive income, and you won't even have to worry about the debt.

It’s a pretty sweet position to be in after about 11 years.

However, the question remains: Is this for everyone?

That’s the question you’re probably asking yourself, saying: Well, can I do this? Is this even worth my time? Is it worth the risk? Or I can't borrow right now, so this doesn’t even apply to me.

Well, that’s correct.

Right now, you can’t borrow, but chances are in the next 12 to 24 months, as rates start cutting, you might be able to. That’s why it’s important to have the strategies in place, the right mindset around mortgages, debt, and how you can actually grow your wealth.

We get taught about reducing our debt all the time—it’s a very defensive play. It would be the equivalent of saying: Look, you have two ways to get rich. Option one is you spend a lot less. Option two is you make a lot more money.”

While you sit there and say: Well, yeah, I’ll just save a lot more and not do those things, for me, life’s very precious. I don’t know when I’m going to fall dead.

As much as I like to prepare and have a nest egg for the future, I still want to enjoy life today. That means I still want my Ben & Jerry’s ice cream (if I can—because, again, calorie deficit and stuff) but if I can go out there and enjoy life, then I want to do that because it makes this whole process more fruitful and sustainable.

That is something I want you to take away from this article: don’t do what the majority of people will do, which is buy a house, pay it off for 30 years, and hope they have enough money to retire.

What you want to do is build an investment portfolio, whether it’s property or something else. If you can leverage your time by outsourcing that to buyers' agents like myself, then you can go out there and do this at speed.

I’ll catch you guys in the next one. Thanks, guys!

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.webp)

.png)

.png)

.png)

.png)

.png)

.png)